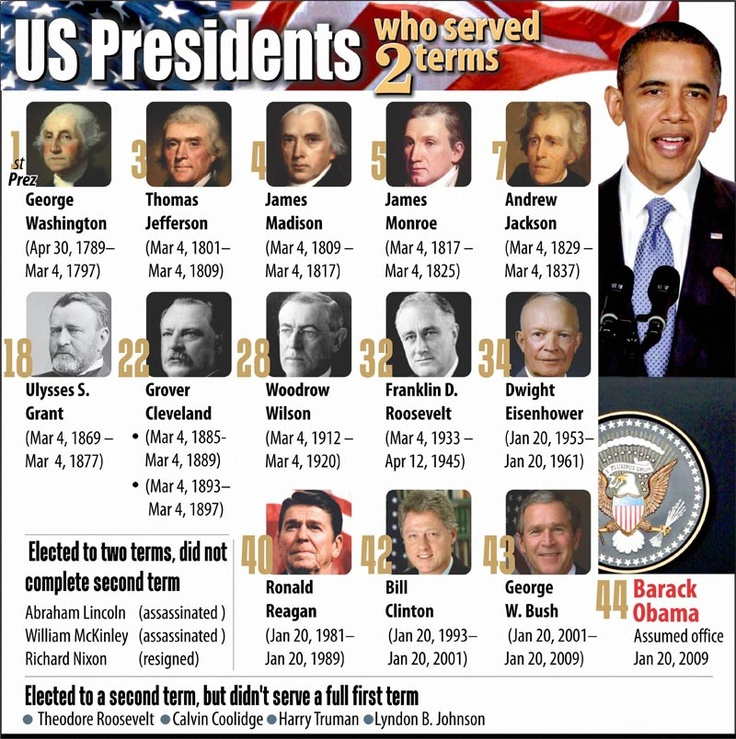

Market news media is buzzing about this, the third year of the presidential cycle, being traditionally the best year in that four year term. While it’s true that the third year is typically the strongest, another perspective is that this is the seventh year in this presidential cycle.

How does the market traditionally react in the seventh year of an eight year cycle? Our research determined that the historical median market gain has been 6%, in the four cases of “year sevens” since the 1951 ratification of the 22nd amendment. While history isn’t guaranteed to repeat itself, overall, it’s typically been a mildly positive year.

Coincidentally, year eight – 2016 for us – has characteristically been the worst market year in all those instances when there has been an eight year presidential cycle. The median loss has been around -6.5% and stock have only been positive in 25% of those instances where an eighth year occurred. If we were to hazard a guess as to why this happens, we’d look to the uncertainty surrounding the final year of a two-term presidency. People wonder what things will look like after the next election; not only who will be in office, but what that will mean for the economy and the markets. This is when people take their money to the sidelines and wait to find out how the new leader will change things.

On top of that, a president in the last year of a second term is not campaigning again. The incentives in year three or four of a single term to take actions that will goose the economy ahead of the next election simply aren’t there. While this president may want to keep his party in power, he’ll be far more concerned about his own legacy. Given the combination of policy tightening in 2015, and 2016 being the final year in a two-term presidency, the end of 2015 is likely to bring serious concerns about market exposure.

– Greg Stewart, CIO

{kind=link}